The 4th AML directive must be implemented across Europe by 26th June 2017 – the European Commission recently announced an AML Action Plan that encouraged territories to fast-track adoption by the end of 2016. The Action Plan suggested we are likely to see a number of changes to the directive this year (largely in light of the Paris terrorist attacks) however no changes have been proposed that will reduce unnecessary cross-border compliance complexity and cost.

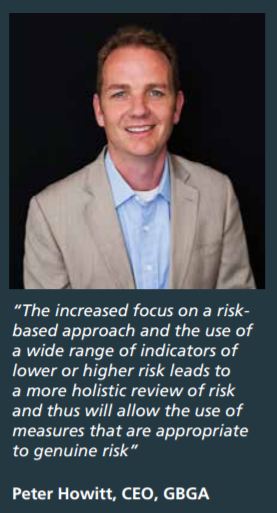

There is much to like about the 4th AML directive particularly with its focus on evidence driven risk-based approaches to AML and counterterrorist financing (CTF). The increased focus on a risk-based approach and the use of a wide range of indicators of lower or higher risk leads to a more holistic review of risk and thus will allow the use of measures that are appropriate to genuine risk. It should also support increased reliance on technological solutions that can improve confidence in customers and transactions, reduce costs and make it easier for good customers to transact (e.g. use of online social identification information and blockchain proof of identity).

That said, the 4th AML directive also represents a huge opportunity missed. Sadly, the on-going European Digital Agenda drive and the need to help small and medium enterprises do business more easily across Europe was completely ignored in the 4th AML directive.

“The lack of harmonisation will lead to increased complexities with little obvious reduction in crime and perhaps the complexity will undermine the purpose of the new regime. The 4th AML directive should have aimed for consistency and ease of compliance for good lawful businesses to work within the EU “

It was time for a more harmonised approach to AML whereby a person that is established in the EEA could comply with local law and be supervised by their Home State regulator (the only sensible solution) for all European transactions and activity. For example, recently the Data Protection Regulation, introduced a so called One-Stop Shop approach which makes the law directly effective (rather than being subject to translation and transposition in each country) and subject to local supervision (but with cooperative articles to help co-ordinate supervisory functions when dealing with other EEA data protection authorities).

Many believe that specific inclusion of online gambling within the 4th AML directive is not particularly burdensome for the sector and a benefit for an industry that often faces hostile political environments. I hope that is true. From my perspective working in the online gambling and the e-payments sectors I have often seen how AML requirements have been used to, or have the effect of, discouraging competition from foreign operators by making it too costly or difficult to operate across borders.

Many believe that specific inclusion of online gambling within the 4th AML directive is not particularly burdensome for the sector and a benefit for an industry that often faces hostile political environments. I hope that is true. From my perspective working in the online gambling and the e-payments sectors I have often seen how AML requirements have been used to, or have the effect of, discouraging competition from foreign operators by making it too costly or difficult to operate across borders.

Many gambling companies are uniquely aware of the importance of Article 56 of the TFEU and the right it gives to provide services across borders. In the financial services sector, the Article 56 right is further enhanced by a passporting process that means you only need to be authorised in one EEA territory to benefit from full cross-border permissions. Yet we have still seen some member states use AML requirements as an effective means to limit supplies of cross-border services (with Germany being the most obvious and egregious example on a number of fronts).

Some of those territories that failed to limit cross-border supply (due to Article 56 rights of operators) may now use the 4th AML directive as an anti-competitive measure. It is harder to persuade a court that a local regulators’ perception of AML and CTF risk should be supplanted by the view of a judge. In addition, the strength of punitive measures available under the 4th AML directive will make challenging unfair local AML requirements difficult.

Under established AML principles, usually the AML law of the EEA territory (Home) where an operator is based applies to its activities but in some territories, the AML provisions of the country where the customer is located may also be applicable (Host). In addition, use of a local agent, a group company and even some commercial partners in another territory will also trigger local AML requirements in the Host territory.

The lack of harmonisation will lead to increased complexities with little obvious reduction in crime and perhaps the complexity will undermine the purpose of the new regime. The 4th AML directive should have aimed for consistency and ease of compliance for good lawful businesses to work within the EU – so that resources could actually be focused on stopping the bad guys and gals.

Structural deficits in the directive and the risk of gold-plating will likely to lead to sectoral discrimination, a lack of coherence in dealing with cross-border conflicts and policy driven rather than risk based rules and enforcement.

There is still time for amendments to the 4th AML directive to enable a coherent European approach to AML and CTF that supports those many good SME’s and cross-border businesses that wish to act responsibility (and not just gambling companies).

In the current economic and political climate we are likely to see the right to do business across borders without unnecessary and unjustified restrictions severely tested, and Europeans need to defend and maintain this right if our grand European project is to succeed.

Source: EGBA News